Managers

Share

Key Takeaways

- Clipper Fund returned +27.43% in 2025 vs. +17.88% for the S&P 500 Index. The fund has consistently grown wealth for shareholders since its inception.

- Short-term forecasts have little predictive value in investing, but we can prepare for the inevitable, including the kinds of market downturns that historically occur with regularity. We believe the best defense is to own durable businesses that can withstand adversity and to acquire them at valuations that leave a margin of safety.

- A prominent risk today is the potential for bubbles in various parts of the market. These include the massive momentum and concentration caused by passive investment flows, the over-valuation of so-called dividend darlings which now face competitive challenges and payout strain, and the hyperactive growth assumptions about anything to do with AI.

- Our highly selective approach in Clipper Fund has enabled us to build a tightly targeted portfolio of companies that combine truly attractive growth and durability with significantly discounted valuations. This gives us the best of both worlds—getting the growth that we seek in long-term investments while avoiding the risk of over-hyped high valuations.

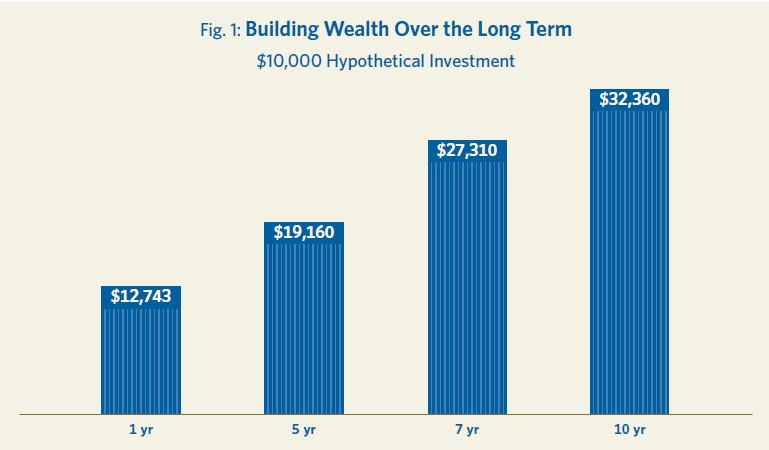

The average annual total returns for Clipper Fund for periods ending December 31, 2025, are: 1 year, 27.43%; 5 years, 13.88%; and 10 years, 12.45%. The performance presented represents past performance and is not a guarantee of future results. The performance presented represents past performance and is not a guarantee of future results. Total return assumes reinvestment of dividends and capital gain distributions. Investment return and principal value will vary so that, when redeemed, an investor’s shares may be worth more or less than their original cost. For most recent month-end performance, click here or call 800-432-2504. Current performance may be lower or higher than the performance quoted. The total annual operating expense ratio as of the most recent prospectus was 0.70%. The total annual operating expense ratio may vary in future years.

This material includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions, or forecasts will prove to be correct. All fund performance discussed within this material are as of December 31, 2025, unless otherwise noted. This is not a recommendation to buy, sell, or hold any specific security. Past performance is not a guarantee of future results. The Attractive Growth and Undervalued reference in this material relates to underlying characteristics of the portfolio holdings. There is no guarantee that the Fund performance will be positive as equity markets are volatile and an investor may lose money.

Performance:

The Power of Active Share

Clipper Fund returned +27.43% in 2025, outperforming the +17.88% return on the S&P 500 Index by almost a thousand basis points. The fund’s performance has been strong over the most recent 5-, 10- and 20-year periods and since inception. It has consistently grown wealth for its shareholders, and a hypothetical $10,000 investment made 10 years previously would have been worth more than $32,000 at the end of 2025.

We achieved these results without having an overweight in the so-called market darlings. For example, our weighting in the so-called Mag 7 stocks is roughly half that of the S&P 500 Index. This is one of the reasons we feel well-positioned for the future—to have achieved such attractive results without being over-exposed to the parts of the market that we consider the most risky, the most overvalued and potentially the most prone to be in a bubble.

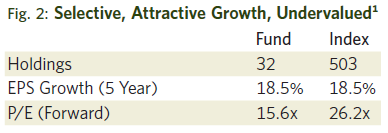

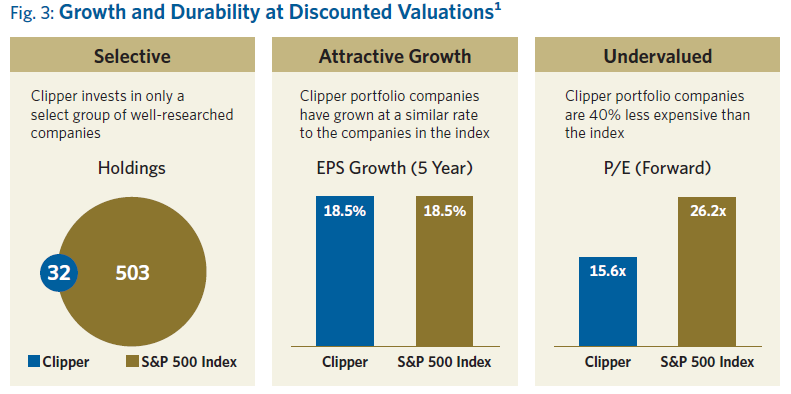

It is a central tenet of our investment approach that we will not look like the index. In the industry this is known as “active share”—in other words, how different are you from the index? Historically we have had a very high active share. By being extremely selective we have been able to construct a tightly targeted portfolio of companies that combines high earnings growth with low valuations relative to the index.

Low valuations are key because buying stocks at prices that leave a margin of safety reduces portfolio risk. Our portfolio is trading at a dramatic discount to the S&P 500 Index despite the attractive earnings growth characteristics of its constituents and the durability of their underlying businesses. This rare combination of attractive growth at bargain prices is what we call a value investor’s dream. It underpins our conviction in the portfolio despite broader concerns about the overall level of hype in the market.

Market Review:

Avoiding Hype, Embracing Realism

When looking at the current investment landscape we emphasize that we are not interested in trying to make short-term forecasts because these have no predictive value. For example, we keep track of the interest rate forecasts of the top Wall Street strategists. We score the forecasts as correct if they get merely the direction right—will interest rates be higher or lower six months from now? Even these experts are wrong almost 60% of the time. Those forecasts have no predictive value.

While we cannot make reliable short-term forecasts, what we can do is prepare for the inevitable. For example, based on historical patterns, investors should expect a market dip of around 5% to happen three times a year and a 10% dip to happen once a year, while on average the market falls 20% or more every three-and-a-half years. Such corrections are painful but they are not a punishment for bad behavior. They are more like an admission fee to the markets, an unpleasant but inevitable part of investing for which we need to be prepared.

With these caveats we can make several working assumptions as we look out at today’s investment and economic landscape. We start with a view that the biggest economic risk we face is monetary inflation. As a country we continue to have the mindset that we can spend more than we make. We have the ability to print money at will, so inflation is an ever-present threat, and one we need to watch closely.

We expect unemployment to trend higher over time. This is partly a reaction to today’s uncertain environment and partly due to the expected impact of AI as it rolls through the economy. We do believe that AI is transformational. Technology has been a key economic driver for the past 30 years, and now AI is an accelerant. Any investment analysis must consider it. However, it has caused perhaps too much excitement and euphoria in the market, not to mention dramatic price moves. We think there are abundant opportunities in AI but the key in this heightened environment is to focus on quality, durability and valuation.

"We should not ignore the hyperactive growth assumptions in the AI space. People are projecting high rates of growth deep into the future, but it is instructive to remember how difficult and unlikely this is."

We do see several potential bubbles as we look at the investment landscape. One concern is the enormous flows into passive strategies which generate massive concentration and market momentum. There is a real risk of a bubble emerging here. We also think there may be shocks and surprises, and disappointed investors, in some of the alternative markets that have less liquidity, whether private equity or private credit.

We also see risk and possible over-valuation when we look at the underlying business fundamentals of some of the so-called dividend darlings. This is an area where people traditionally feel safe, but payout ratios are stretched and many of these businesses that were once considered stalwarts now face competitive challenges.

Talking of possible bubbles, we should not ignore the hyperactive growth assumptions in the AI space. People are projecting high rates of growth deep into the future, but it is instructive to remember how difficult and unlikely this is. The race is not always to the swift nor the fight to the strong, as they say, but that seems to be the way people are betting. We are probabilistic investors and look at the odds against companies maintaining high growth rates for long periods of time. The analysts who are projecting high growth rates for these companies also assume they will somehow sustain very rich margins indefinitely rather than see them competed away. It is an unlikely outcome. We believe some investors are headed for disappointment with their rosy outlooks for many of the AI companies.

As we look at the investment landscape broadly, we consider it prudent to prepare for the sorts of normal volatility and shocks that appear over a long investment cycle. We make sure that we stress-test all the companies in our portfolios against material market corrections and economic recessions. We do not know when a recession will come, but we know that one will come eventually, and we need to be ready for it. We know too that there can be geopolitical shocks which, by nature and definition, are unpredictable. At present we are in an environment of enormous political and fiscal uncertainty. Investors should not be pessimistic but they should be realistic. The key is to mitigate risk and focus on companies with the durability, quality and ability to get through the inevitable shocks that we will face in the years ahead.

Portfolio Notes:

Building Confidence from Conviction

Here we look at the major elements of the Clipper Fund portfolio, the specifics of our positioning and the themes and sectors and companies where we see the biggest opportunities in today’s market.

In technology we have achieved good results despite being significantly underweight in some of the Mag 7 stocks that have been driving the market. The key is to be highly selective within this sector which has attracted so much hype. Our focus is on valuation. We do not want to buy the companies that are overvalued with hyperactive growth assumptions. We do want to focus on the stalwarts as distinct from the concept companies and the market darlings.

One area of focus is the companies that combine the raw materials of massive compute capacity with enormous data sets. They have the customer bases and the cash flow that allows them to make investments in core capacity without taking on large debt leverage or constantly issuing equity, as some of the darlings have done. Meta and Alphabet are two examples of companies we own that have these ingredients. So too is Amazon in a different way—it is an enormous provider of compute, a beneficiary of the shift to agentic AI and one of the best managed and most durable companies in this sector.

Within the AI world, we also focus on the companies that make the picks and shovels. One example in our portfolio is Applied Materials—it makes the equipment that makes the chips. Another is Texas Instruments, not a household name but on the leading edge of tech innovation as it manufactures the essential nuts and bolts of the systems being created to move us into this brave new world.

Our technology holdings were big contributors to our 2025 results. Based on the strong market gains, we trimmed certain holdings like Meta and Applied Materials. We consider these companies very attractive but must stick to our valuation discipline since, as prices run ahead, the margin of safety shrinks. We used the proceeds from sales to add to our positions in certain overlooked technology names like Pinterest.

Financial stocks have been getting a lot of attention in the market lately. We have believed for more than three decades that selectivity is the key to investment in this sector. It is not a sector that you want to index. You want to own those companies that are competitively advantaged and have the sort of characteristics that we call growth stocks in disguise. Selectivity and differentiation really pay off in this sector as we continue to see a tale of two cities—on one hand, those companies that are positioned for the changes ahead and, on the other hand, those companies that will inevitably be disadvantaged.

We like financial companies that are positioning themselves to reap the benefits of AI, and have the scale and the mindset and the data to do it well. These include banking giants like Capital One, Wells Fargo and U.S. Bancorp with their deep nationwide customer bases. It includes Markel, a specialist insurer where AI can potentially play a major role in risk analysis and pricing. It includes Berkshire Hathaway, notable for its durability and breadth.

The selective financials we own outperformed the financial sector as a whole. They were significant contributors to our results, and we used that strength to trim our exposure in businesses where we believed the margin of safety was being reduced.

Healthcare is an industry where there has been enormous volatility by sub-sector and by company, and the key again is to be opportunistic. We focus on companies we consider recession-resistant—those that have the characteristics of durability and strong sustainable demand. We like those parts of the industry that concentrate on services and generic pharmaceuticals and we avoid companies with big single drug exposures and similar risks.

In this sector too we want to own businesses that can use AI to enhance earnings by reducing costs and improving the customer and patient experience. Our portfolio holdings include CVS Health, which has a very broad and resilient portfolio across healthcare services and products. We own Viatris, a maker of branded generics, not a glamorous business but a durable, reliable and steady source of cash flow. We also own Solventum, formed when 3M spun out its healthcare products business in 2024, and another example of durability in healthcare.

In commodities, while gold and other precious metals captured the headlines we have focused on undervalued energy and materials companies. Oil has been somewhat overlooked in this commodity boom, and we have taken the opportunity to selectively add companies like ConocoPhillips to the portfolio. Another major theme is the shift towards electrification and the increased demand for power that it entails. We have a holding in Coterra Energy, a company known for its strong presence in natural gas in the Marcellus Shale in Pennsylvania as well as its core holdings in the Permian Basin in Texas. These deep, cheap sources of natural gas give it an advantage as a provider of the fuel that will support the transition to renewable energy. Electrification also means increased demand for copper, a key element in power transmission and other electrical applications. We own Teck Resources, a Canadian firm that has some of the most long-lived and lowest-cost copper reserves in the world.

Finally, a key category in our portfolio is what we call oversold and under-earning. We could also call this group “the overlooked” but, as value investors, want to make sure to avoid value traps. These are businesses that have durability in the sense that they are not likely to be disrupted and can withstand cyclical downturns while, at the same time, are attractively valued on somewhat depressed earnings. They may be under temporary or cyclical earnings pressure. This gives us two ways to win potentially—a recovery in earnings and an upgrade in market valuation. We can mention two poster children for this theme in the portfolio. One is Tyson Foods, in reality the largest protein producer in America, supplying both chicken and beef on a mass scale. Another is MGM Resorts, one of the largest casino operators in the world which owns properties in Las Vegas and Macau and is developing what we expect will be the most valuable gaming asset in Japan, set to open by the end of this decade.

This gives a sense of how our portfolio is positioned both by theme and, more importantly, by the very specific types of companies that we own to take advantage of our core investment tenets in this fast-changing economy.

One of the key characteristics of the current market environment is the bipolar nature of investor sentiment. On one hand there are the wild optimists who believe we have reached a plateau of permanent prosperity; they are chasing momentum and growth and taking enormous risks. On the other hand are those investors who are terrified and bearish and pessimistic, and who think the market has come too far too fast. They want to wait on the sidelines. Of course, the risk they take is that they miss out on being invested for the long term.

We try to build our portfolio based not on being optimistic or pessimistic but being realistic. We look for a portfolio that can withstand the inevitable shocks but also make progress when times are good without taking on big momentum risks. Our extreme selectivity allows us to identify just a handful of companies that combine truly attractive growth and durability with significantly discounted valuations (see Figure 3). Owning above-average companies at below-average prices gives us the best of both worlds—getting the growth that we seek in long-term investments but avoiding the risk of over-hyped high valuations.

This is how we are building the Clipper Fund portfolio in today’s uncertain world. As a result, while we express our concern and caution about the current market euphoria, we have great confidence and conviction in how we are positioned for 2026 and beyond.

Together on This Journey

For more than 50 years, Davis Advisors has navigated a constantly changing investment landscape guided by one North Star: to grow the value of the funds entrusted to us. We are pleased to have achieved strong results thus far and look forward to the decades ahead. With more than $2 billion of our own money invested in our portfolios, we stand shoulder to shoulder with our clients on this long journey.2 We are grateful for your trust and are well-positioned for the future.

Five-year EPS Growth Rate (5-year EPS) is the average annualized earnings per share growth for a company over the past 5 years. The values shown are the weighted average of the 5-year EPS of the stocks in the Fund or Index. Approximately 2.60% of the assets of the Fund are not accounted for in the calculation of 5-year EPS as relevant information on certain companies is not available to the Fund’s data provider. Forward Price/Earnings (Forward P/E) Ratio is a stock’s price at the date indicated divided by the company’s forecasted earnings for the following 12 months based on estimates provided by the Fund’s data provider. These values for both the Fund and the Index are the weighted average of the stocks in the portfolio or Index.

As of 12/31/25, Davis Advisors, the Davis family and Foundation, our employees, and Fund trustees have more than $2 billion invested alongside clients in similarly managed accounts and strategies.

This material is authorized for use by existing shareholders. A current Clipper Fund prospectus must accompany or precede this material if it is distributed to prospective shareholders. You should carefully consider the Fund’s investment objective, risks, fees, and expenses before investing. Read the prospectus carefully before you invest or send money.

This material includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions or forecasts will prove to be correct. These comments may also include the expression of opinions that are speculative in nature and should not be relied on as statements of fact.

Davis Advisors is committed to communicating with our investment partners as candidly as possible because we believe our investors benefit from understanding our investment philosophy and approach. Our views and opinions include “forward-looking statements” which may or may not be accurate over the long term. Forward-looking statements can be identified by words like “believe,” “expect,” “anticipate,” or similar expressions. You should not place undue reliance on forward-looking statements, which are current as of the date of this material. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. While we believe we have a reasonable basis for our appraisals and we have confidence in our opinions, actual results may differ materially from those we anticipate.

Objective and Risks. The investment objective of Clipper Fund is long-term capital growth and capital preservation. There can be no assurance that the Fund will achieve its objective. Some important risks of an investment in the Fund are: stock market risk: stock markets have periods of rising prices and periods of falling prices, including sharp declines; common stock risk: an adverse event may have a negative impact on a company and could result in a decline in the price of its common stock; financial services risk: investing a significant portion of assets in the financial services sector may cause the Fund to be more sensitive to problems affecting financial companies; focused portfolio risk: investing in a limited number of companies causes changes in the value of a single security to have a more significant effect on the value of the Fund’s total portfolio; foreign country risk: foreign companies may be subject to greater risk as foreign economies may not be as strong or diversified. As of 6/30/26, the Fund had approximately 14.1% of net assets invested in foreign companies; headline risk: the Fund may invest in a company when the company becomes the center of controversy. The company’s stock may never recover or may become worthless; large-capitalization companies risk: companies with $10 billion or more in market capitalization generally experience slower rates of growth in earnings per share than do mid- and small-capitalization companies; manager risk: poor security selection may cause the Fund to underperform relevant benchmarks; depositary receipts risk: depositary receipts involve higher expenses and may trade at a discount (or premium) to the underlying security and may be less liquid than the underlying securities listed on an exchange; fees and expenses risk: the Fund may not earn enough through income and capital appreciation to offset the operating expenses of the Fund; foreign currency risk: the change in value of a foreign currency against the U.S. dollar will result in a change in the U.S. dollar value of securities denominated in that foreign currency; and mid- and small-capitalization companies risk: companies with less than $10 billion in market capitalization typically have more limited product lines, markets and financial resources than larger companies, and may trade less frequently and in more limited volume. See the prospectus for a complete description of the principal risks.

The information provided in this material should not be considered a recommendation to buy, sell or hold any particular security. As of 12/31/25, the top ten holdings of Clipper Fund were: Capital One Financial, 9.29%; Alphabet, 7.58%; Markel Group, 6.70%; Meta Platforms, 6.52%; U.S. Bancorp, 5.59%; Berkshire Hathaway, 5.29%; Applied Materials, 5.13%; MGM Resorts International, 4.89%; CVS Health, 4.57%; and Coterra Energy, 3.61%.

Clipper Fund has adopted a Portfolio Holdings Disclosure policy that governs the release of non-public portfolio holding information. This policy is described in the prospectus. Holding percentages are subject to change. Click here or call 800-432-2504 for the most current public portfolio holdings information.

Clipper Fund was managed from inception, 2/29/84, until 12/31/05 by another Adviser. Davis Selected Advisers, L.P. took over management of the Fund on 1/1/06.

The Global Industry Classification Standard (GICS®) is the exclusive intellectual property of MSCI Inc. (MSCI) and S&P Global (“S&P”). Neither MSCI, S&P, their affiliates, nor any of their third party providers (“GICS Parties”) makes any representations or warranties, express or implied, with respect to GICS or the results to be obtained by the use thereof, and expressly disclaim all warranties, including warranties of accuracy, completeness, merchantability and fitness for a particular purpose. The GICS Parties shall not have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of such damages.

The “Magnificent 7” is a group of seven dominant, high-performing U.S. technology companies that have a significant influence on the stock market. The companies that make up the Magnificent 7 are: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla.

We gather our index data from a combination of reputable sources, including, but not limited to, Lipper, Clearwater Wilshire Atlas and index websites.

The S&P 500 Index is an unmanaged index that covers 500 leading companies and captures approximately 80% coverage of available market capitalization. Investments cannot be made directly in an index.

After 4/30/26, this material must be accompanied by a supplement containing performance data for the most recent quarter end.

Item #4768 12/25 Davis Distributors, LLC, 2949 East Elvira Road, Suite 101, Tucson, AZ 85756, 800-432-2504, clipperfund.com

Clipper Fund

Annual Update 2025

Managers